The last few years have seen subscription-based business models gain traction across various sectors. One area that we think has plenty of unrealised potential is financial services.

On one hand, there’s nothing new about recurring fees in banking products. For example, in the 1990s many high street banks in the UK began to differentiate by offering accounts that charged a monthly fee to access bundles of services (e.g. preferential access to other products, travel insurance, breakdown recovery, etc).

However, there is more to subscriptions than charging people by the month. As we’ve explored in previous blogs, the subscription mindset requires a shift to customer centricity. The real opportunity is for financial services to use subscriptions to move beyond product-centric ways of thinking, and focus on building lifetime value for customers.

In this article, we examine how financial services are starting to gain inspiration from the current boom in subscription-based models.

1. Neobanks like Monzo are remarketing ‘fees’ as ‘subscriptions’ and putting customer needs at the heart of their tiered value proposition

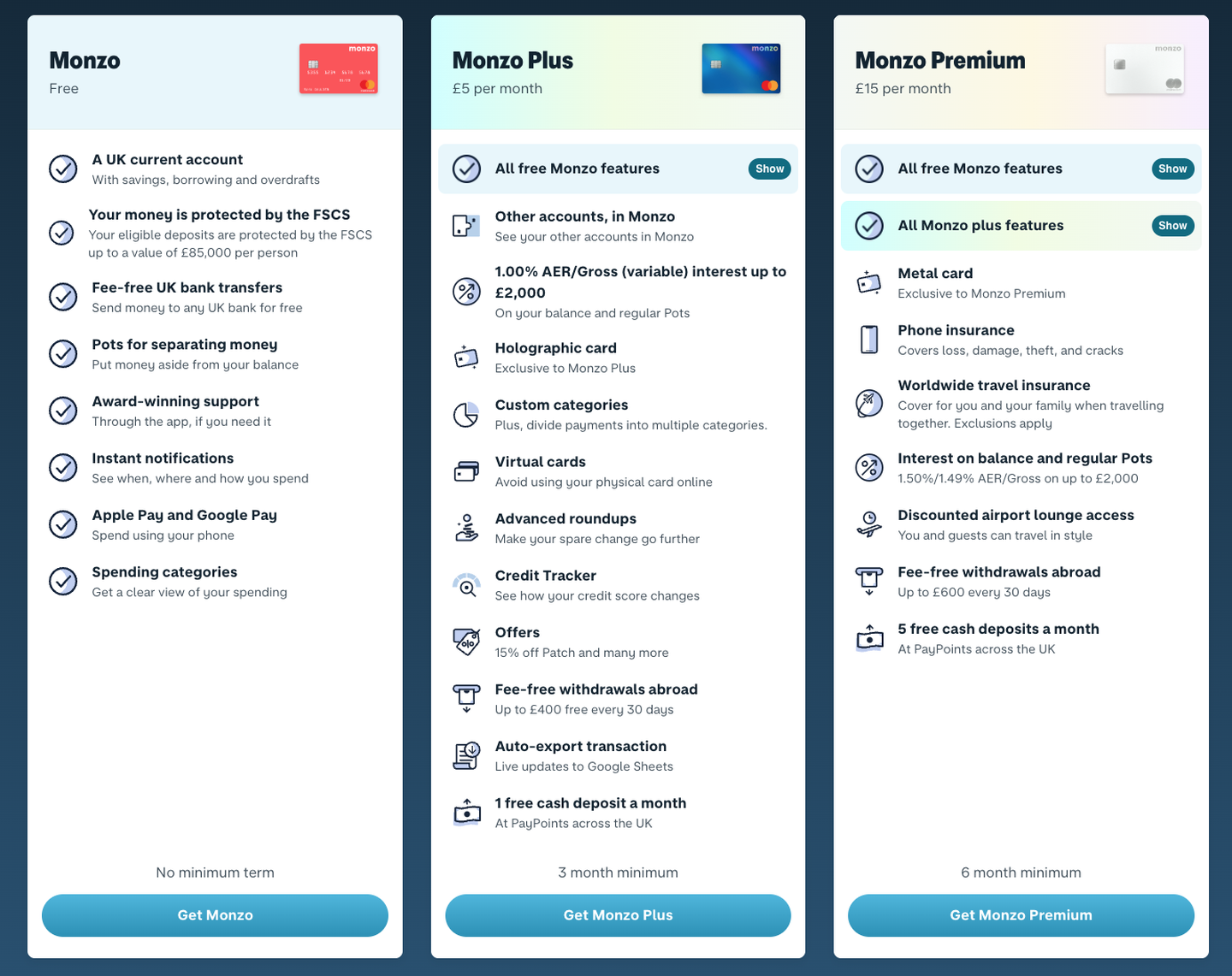

Neobanks have been leading the way in borrowing from the world of subscriptions in both their marketing and product design. It’s interesting to compare the fee-charging premium accounts offered by a neobank like Monzo, with the offer put forward by most traditional banks.

Traditional banks typically have a large number of accounts on offer, with customers asked to choose from as many as six or seven account types. Often, these accounts are not clearly differentiated, with complexity introduced by overlapping price points, inconsistent naming and unclear benefits. The language used is interesting too – in many cases, we have seen banks refer to a ‘monthly fee’ (language rarely used by successful subscription businesses).

In contrast, Monzo clearly presents three tiers of progressive value, at a smart range of price points (free, £5 and £15). Each tier is clearly differentiated, with premium benefits added to those offered in the tier below. This approach has become considered best practice for digital subscriptions, having been adopted and tested by many leading media and SaaS services in recent years.

There are also important differences in the type of value proposition offered across each tier. Traditional banks typically base their premium value proposition on additional services bundled with the bank account itself (e.g. travel insurance, breakdown cover and mobile phone insurance). Conversely, Monzo has built tiers largely around product features central to a customer’s banking experience. These include: seeing third-party bank balances in Monzo, a holographic payment card, the ability to create custom categories, fee-free withdrawals abroad and an auto-export to Google Sheets function.

Customer-centric subscription businesses like Monzo focus more on the value their product can add to someone’s life, and much less on the cost savings they can offer by providing discounted access to unrelated services.

Recasting a paid service as a subscription is not unique to retail banking. Charles Swabb has had huge success by reimagining an existing financial planning service as ‘Schwab Intelligent Portfolios Premium’. This simplified value proposition offers two tiers: free and premium. The premium tier’s core value proposition is the offer of unlimited 1:1 guidance from a Certified Financial Planner, in exchange for a $30 monthly subscription. Within four months of launching, the product had attracted $1bn assets under management.

FT Strategies insight: When offering products with recurring fees, financial organisations should keep things simple. Don’t overwhelm or confuse your customers with multiple tiers. And create a value proposition that focuses on the primary job that people use your product for.

2. Corporate banking services like Nordea’s AutoFX show how technology-driven innovation can change transactional customer relationships into ongoing outcome-based ones

Corporate banking offers many services that can be reconsidered through the subscription lens. One example is AutoFX Liquidity Management, a forex solution being offered to clients by Nordea. AutoFX provides automated sweeping (exchange positive balances on your currency accounts to your desired levels and desired currency), automated topping (top up your currency accounts to a desired level through exchanges from your chosen currency), and can perform overnight swaps in order to reduce the eliminate negative balances on foreign currency accounts (and therefore prevent unnecessary interest costs).

Jean-Francois Tapprest, Large Corporates & Institutions (LC&I) Business Innovation Lead at Nordea, has described Nordea AutoFX as ‘a subscription in disguise’. Automated services like AutoFX are one way that Nordea has started to focus on long-term relationships with customers. Rather than a big upfront fee, payments flow in a pay-as-you-go manner. And by focusing on helping customers achieve an outcome, Nordea’s forex business is shifting from a product-centric business model to a customer-centric one.

In the world of corporate banking, this represents a substantial change in mindset, as Tapprest explains: “In daily corporate banking, most products are rather commoditised with many pricing metrics dictated from the outside (interest rates, standard market practices, etc.) resulting in a lower control over the business model. The pricing of those commoditised products is not value-based (or value-centric) … Adopting a subscription mindset involves shifting from the logic of selling products to that of offering a subscription to services.”

As such, subscriptions offer one way for corporate banking to escape commoditisation and truly differentiate the type and level of service provided.

FT Strategies insight: Technological developments are creating countless opportunities for product innovation (e.g. automation of previously manual processes). Being customer-centric instead of product-centric, focusing on the bigger customer problem you are trying to solve and fostering a long-term relationship with your customers can maximise the value created by a new product, and offer opportunities to iterate its business model.

3. Financial services are expanding their traditional core products by offering new ecosystems of services, often via subscriptions

One of the successful features of subscriptions like Amazon Prime is the ability to offer value across a company’s group of services (e.g. Amazon Music, Audible, free next-day delivery, photo storage). We’ve seen several financial businesses create ‘one-stop-shop’ bundles that aim to provide value beyond the scope of a traditional core product.

For example, neobanks like Tide and Holvi offer subscription-based services for self-employed and small business owners. Their offerings bundle banking with additional functionality that solves specific challenges faced by small businesses. For example, both services allow customers to create, send, track and store invoices online. They also provide services that assist with bookkeeping (e.g. receipt scanning, expense categorisation, and exportable documents including income statements and VAT reports).

Traditional banks have also started to move in this direction, creating value-add ecosystems that cross over into non-financial services. For example, Singaporean bank DBS has started to offer SME’s a wider package of digitalisation as part of its Start Digital offer. DBS describes their role in this business transformation proposition as ‘more like a partner, less like a bank’. Start Digital is a subscription bundle offering customers a wide range of support, including tax services, online HR and cybersecurity tooling. This support is delivered via an ecosystem comprising third-party partners (e.g. cloud accounting provider Xero) and DBS’s own products (e.g. DBS MAX, an end-to-end cash collection system).

Insurers have also seen the potential of moving into adjacent subscription services. For example, Spanish multinational insurance company MAPFRE has launched a digital health subscription platform called Savia. Savia offers people an in-person and online consultation service to provide on-demand access to medical specialists and third parties. Pedro Díaz Yuste, Head of Digital Health at Mapfre, explains: “Savia is not digital insurance for health, it is a digital platform for health services… we integrate digital services from third parties in an easy way, in order to provide our customers with the best solutions in digital health”. In its first three years of operation, Savia had reached more than 380,000 users with 75,000 active customers.

FT Strategies insight: Service ecosystems provide financial service businesses with a unique opportunity to monetise and differentiate their offerings. Reimagine your role as one of a ‘trusted partner’, and focus on providing services that meet your customer’s wider needs. Partnerships offer a simple way for financial organisations to broaden their offer beyond their own specialisms.

FT Strategies can help you explore the subscription opportunity for your business

We’ve worked with a range of financial services businesses to develop subscription strategies. So whether you are considering a change to your current business model, or launching a new service that complements your existing products, we can help you navigate the opportunity. We invite you to get in touch if you’d like to continue the conversation.